Dear Friends,

I hope this email finds you and your families enjoying the Spring in good spirits!

In the wake of Monday's news on the JPMorgan Chase takeover of First Republic, yesterday the Fed announced a key interest rate increase of 0.25 points, making this the 10th hike in the last 14 months and pushing its target range to between 5% and 5.25%. The good news appears to be that the Fed also hinted this rise may be its last for the time being. With all of these big headlines, I thought it opportune to furnish you now with a comprehensive analysis of the Manhattan real estate market, its trends and my observations and thoughts.

The last 30 days have seen excellent activity throughout the market -- in my own business, I have negotiated 7 deals and submitted 5 purchase applications. In fact, just two weeks ago I received multiple full-ask offers on a listing after just three weeks on the market, confirming the market's readiness to absorb good property that has been prepared, priced and marketed with expertise. As a seasoned professional who transacts at volume in a range of price points, neighborhoods and product types, I regularly review a variety of sources for the most comprehensive pulse on the market.

Accordingly, I have crafted the below drawing from Brown Harris Stevens' weekly Contracts Signed Report, First Quarter Manhattan Residential Market Report for 2023, April Inventory Report as well as data on signed contracts for the Upper Luxury segment of the market ($4M+) from the Olshan Report which I closely monitor. In your review of the below, it's important to note that while the residential sales market has cooled since the frantic pace we saw in 2021 and the beginning of 2022, we are in fact outperforming the pre-pandemic years in spite of interest rate hikes, inflation and bank failures. There were 2,699 closings reported in the first quarter of 2023, making our current market about8% more active than the pre-pandemic years (2018 - 2020) when the first-quarter average was 2,502 closings.

It is my hope that you will find this assembly of data points and ensuing analyses useful in what may seem like uncertain times as you weigh your needs, be they immediate or just for information. In your review of the below, should you wish to receive any of the reports here referenced in their entirety, would like any further detail on the information here enclosed or have any needs or questions for which I can be of service, please don’t hesitate to call.

With all my best wishes,

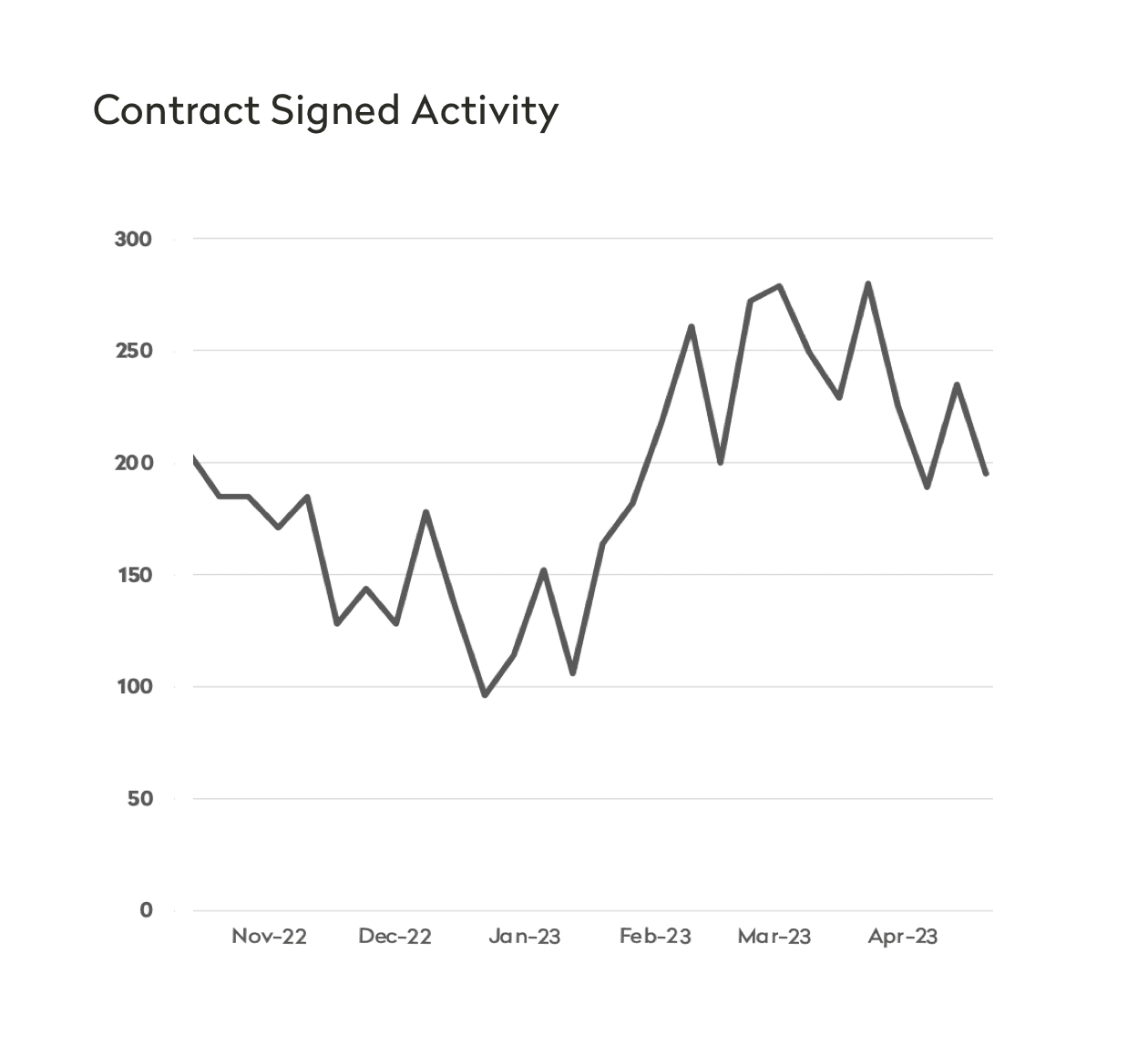

The Overall Market

Market activity is now much more closely resembling seasonal norms. Last week saw a pop in new development with 30 signed contracts, up from 21 contracts the week before for a 43% weekly change. Resale, however, lagged with 165 signed contracts last week compared to 214 signed contracts the week before.

That said, the average asking price for resale property that went into contract last week was $2,172,018 compared to $1,669,535 for the same period last year, representing a 30% increase year over year. That uptick is due to a sizable increase in the number of apartments in the $2M - $3M range that went into contract last week, a price category that has otherwise been sluggish.

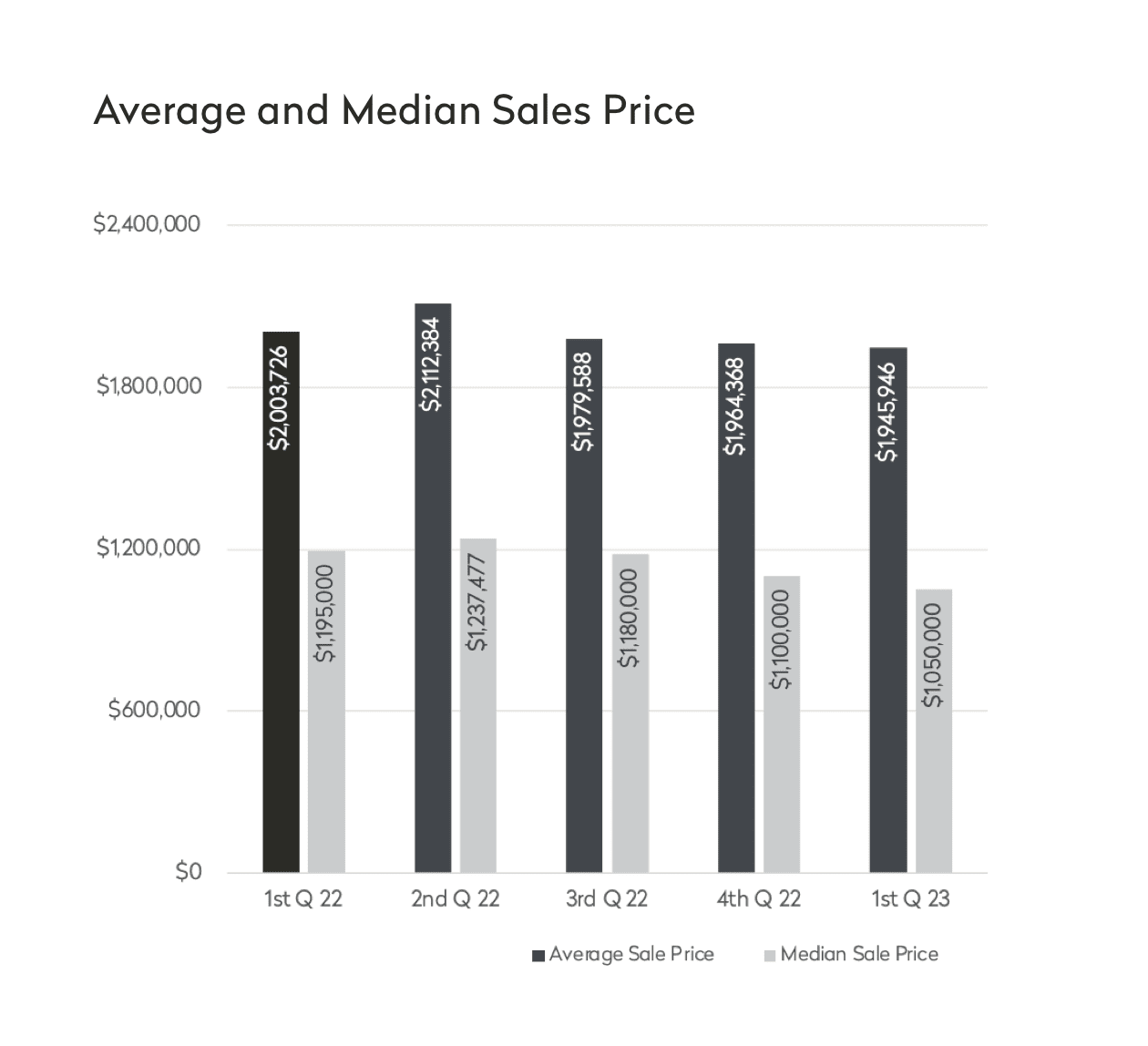

Putting those weekly averages into context with the market at large, the average Manhattan apartment sales price in Q1 2023 was $1,945,946 in Q1 2023 which was consistent with where average sales prices were in Q4 2022 when they were $1,964,368. The average apartment sales price declined approximately 3% from Q1 2022 when it was $2,003,726. The median sale price fell 12% from last year to $1,050,000 from $1,195,000 which is likely in great part representative of the slowdown in the upper luxury segment of the market we’ve seen over the past year.

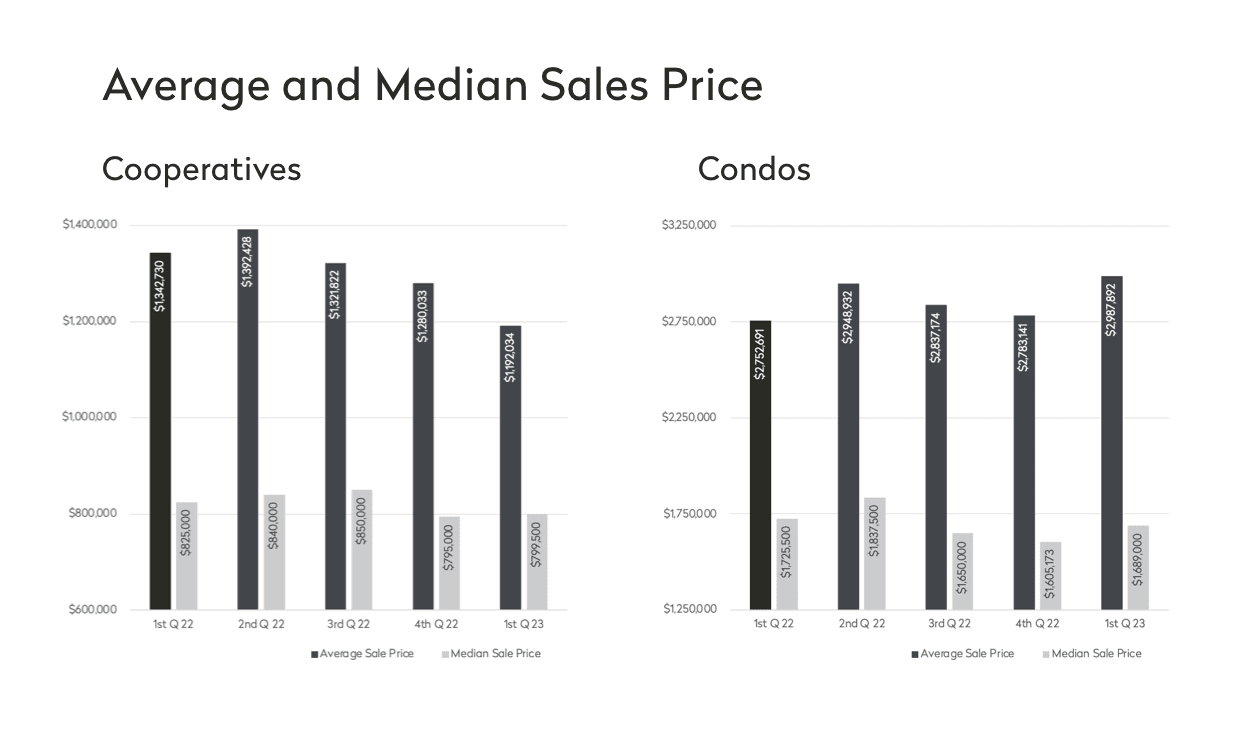

We are now seeing increased softness in cooperative apartments compared to condos which is isn’t surprising as the typical condo comes with more amenities and newer finishes with fewer rules and more flexibility in ownership structure and financing which is more attractive to buyers looking for value. While it’s too early to say whether or not this will be a trend that continues, the opposite directions in which average prices for cooperatives and condominiums have moved since last year is something to keep an eye on. Last quarter every size category of cooperative apartments saw lower sale prices as the average price of a cooperative apartment in Q1 2023 fell to $1,192,034 from $1,342,730 last year, representing a 13% decrease year over year.

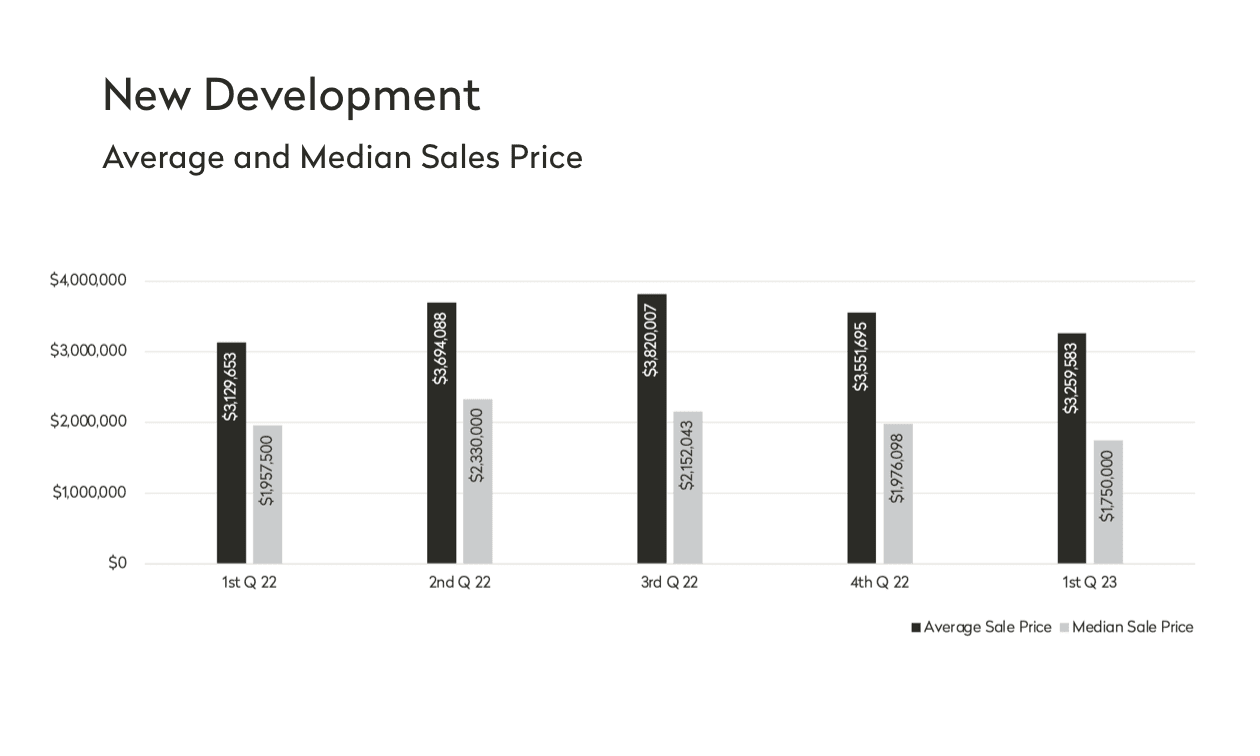

By contrast, the average condo sold for $2,987,892 in Q1 2023 representing an 8% increase from last year when it was $2,752,691. This rise was driven in great part by 3+ bedroom condo resale prices which were up 24% to $6,085,897 in Q1 2023 from $4,923,006 last year as well as new development sales which averaged $3,259,583 in Q1 2023, up 4% from last year when they averaged $3,129,653.

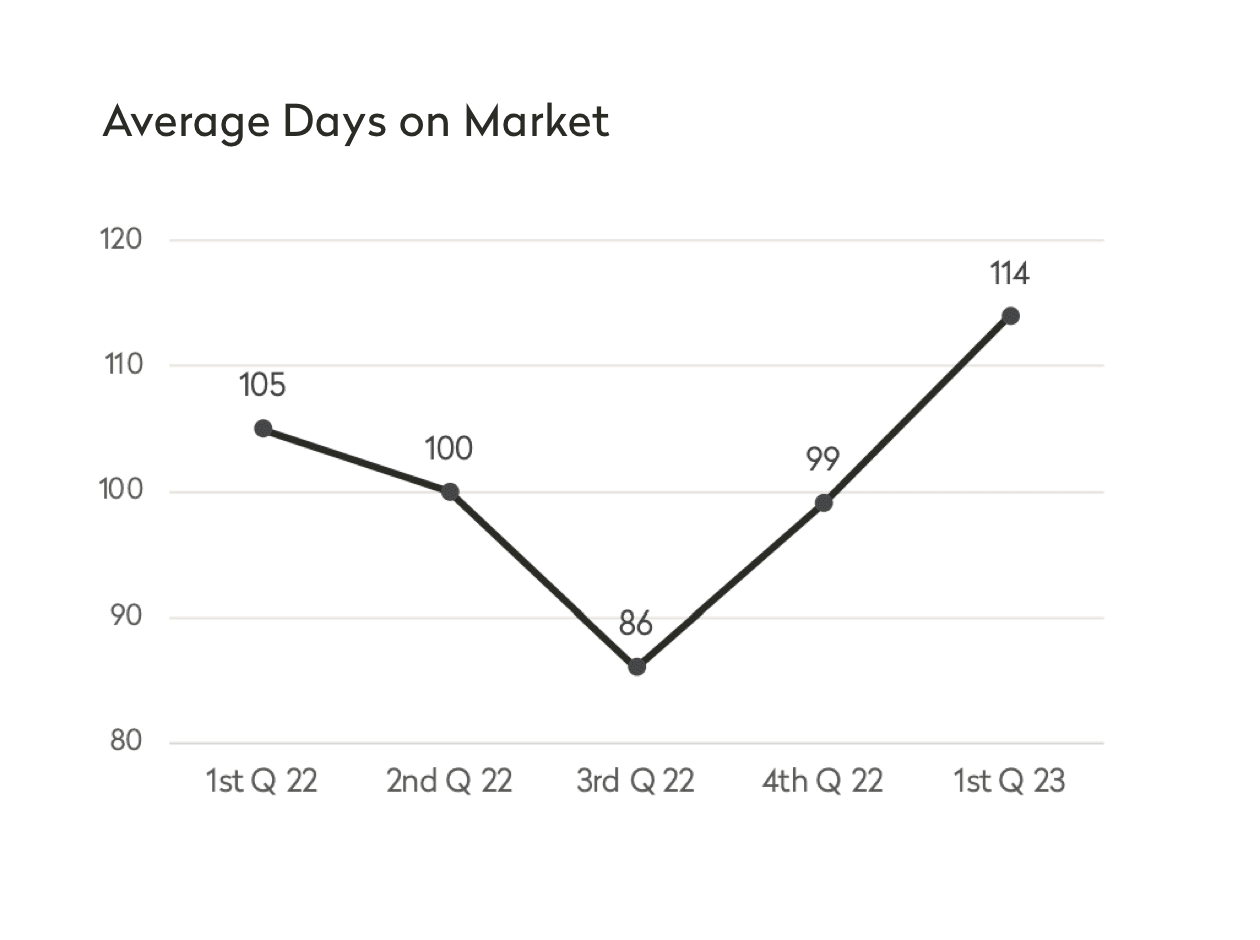

As for activity, as noted above there were 2,699 closings in Q1 2023 which represents a 33% drop from last year when there were 4,023 closings during record levels of activity. That said, activity in Q1 2023 was in line with the pre-pandemic years (Q1 2018-2020) when there were an average of 2,502 closings. With regard to how quickly property is trading, inventory has been increasing steadily since January of this year and so it’s not surprising that last quarter we saw a higher average for days on market at 114 days, up from 99 days in Q4 2022 and 105 days in Q1 2022. To that end, we’ve also seen greater flexibility from sellers as sale prices achieve on average 97.4% of last asking price, down from last year when they achieved 98%.

Upper Luxury: $4M+

Reviewing activity in the Upper Luxury segment of the market, there have been on average 29 contracts signed per week for the month of April for apartments $4M and up. This represents approximately a 28% drop in contract signings from the same period in 2022 when there were 37 contracts signed per week during a period of heightened activity throughout the market which is closely in line with the overall market pullback we saw by the end of Q1 2023. Diving deeper into the numbers, it’s worth noting that in the Upper Luxury segment of the market the asking price volume over the past month dropped to an average weekly total of $209,260,125 from $301,800,594 in April 2022.

Last week (4/24 – 4/30) was a big one in Upper Luxury – we saw an asking price sales volume of $284,790,000 which is the highest weekly total recorded in 12 months, since the corresponding week of 2022 (4/25 – 5/1) when the total asking price volume was $287,014,000. Among the 27 contracts signed last week were 11 properties with asking prices of $10M and above – the largest number of properties at that price point to go into contract since the week of December 20, 2021.

Inventory

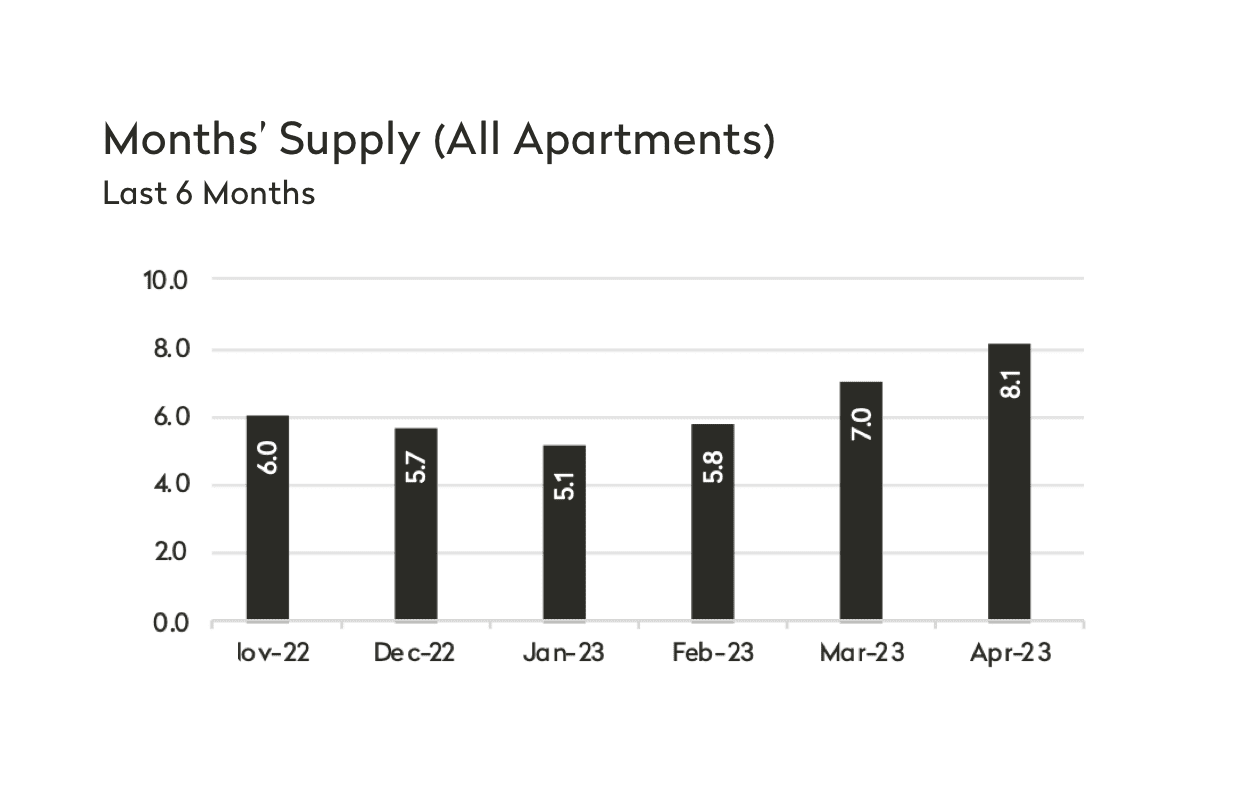

As we start off May, we do so in a market that is skewing in favor of buyers as supply rates reach their highest levels since June 2021. Manhattan had an 8.1-month supply of apartments for sale in April, up 15% for condos and 18% for coops from March. That said, I just received a signed contract with multiple offers at full ask on one of my East Side cooperative exclusive listings after only a couple of weeks on the market which is affirmation that regardless of supply rates good product trades fast and well when presented and priced properly. Buyers are always waiting in the wings to scoop up good property when it hits the market.

A few highlights for you:

- Overall, 3+ bedroom condos were the most abundant property type with a supply rate of 12.4 months. .

- Supply was lowest again Downtown between 14th and 34th Street at 6.7 months, followed closely by the West Side at 7.2 months.

- The most oversupplied neighborhood was again Midtown West at 11.2 months.

Sumamry

In conclusion, despite a less than ideal economic landscape and a couple of headlines, our current market is resilient. In my own business, I'm actively negotiating deals and moving inventory, and there is in fact momentum as we push more deeply into the Spring market. Life-cycle motivated buyers are now feeling the pressure to make moves, having delayed their plans for the last year. For those of you in the market to buy, inventory is trending upward and there are great deals to be had with motivated sellers. To those considering selling, there remain many buyers who have been waiting on the sidelines in anticipation of new property coming to market who are ready to make offers. The market in fact remains abundant with opportunity for all.

I so hope the above feedback has been useful to you, and please don’t hesitate to get in touch with questions or requests for copies of any of the reports referenced in this analysis. As you consider your needs, be they immediate or for continued information, I hope that you will continue to think of me as your expert and that you won’t hesitate to reach out to me with any real estate needs that you may have.

Warmly,